How to leave a winning company you built (on purpose)

Most founder CEO transitions happen because something breaks. Mine happened because everything was working.

2026 arrived, and Jones was doing great. We had been building a vertical software company for 9 years, and we were hitting our stride.

Q3 and Q4 of 2025 were our largest quarters in revenue history. We had crossed the 8-figure ARR milestone while doubling our sales and marketing efficiency and slashing monthly burn by 65% year over year. We’d just shipped the industry’s first AI Insurance Agent. We had 231 people across four global offices, protecting over 36,000 projects and properties from insurance risk across 2.7 billion square feet of real estate and construction.

And I handed over the CEO role to someone else.

If that sounds counterintuitive, it should. The conventional wisdom says founders step back when things get hard. A couple of missed quarters. An exhausted leader. A Board running low on patience.

I’m here today to argue the opposite: the best time to make a founder-led CEO transition is when things are working. And I want to share exactly how we pulled it off.

Table of contents:

My company became the market leader

When private equity entered the picture

Three signals that it is time to transition

The mechanics of a clean CEO transition

My company became the market leader

In February 2017, my Co-Founder and CTO, Michael Rudman, and I won the AXA InsurTech Competition in Tel Aviv. We had a simple idea with a complex execution problem: construction and real estate companies were drowning in insurance paperwork, taking on enormous legal and financial risk because the process of verifying that contractors and vendors held the right insurance coverage was entirely manual, slow, and error-prone.

We believed AI could solve it, and most people in the industry had never thought about the problem long enough to disagree. But at the time, AI models were neither accurate nor sophisticated enough to solve the problem end-to-end. We made a bet on building the AI future.

What followed was nine years of building from scratch, shaping the category before the category had a name, and before AI took over the narrative in tech. We survived fundraising winters. We navigated a global pandemic. We dodged a national banking crisis. We made hundreds of wrong bets and a handful of right ones that defined our trajectory. The early years were a relentless test of whether the vision was real or whether we were just stubborn enough to keep believing in it.

By late 2025, the answer was clear: Jones had become the market leader for insurance verification in the built world, serving the country’s largest construction and real estate companies. Customers trusted us with their most critical workflows every day, at a scale I hadn’t dared to think about in 2017.

This is the company I handed off to a new CEO.

When private equity entered the picture

The chapter that most directly shaped the CEO transition wasn’t the product milestones or the record revenue achieved. It was the shift in our capital structure and one specific moment in Q1 2025 that made everything clear.

When a private equity group joined as our institutional partner in November 2024, it marked a meaningful transition in the company’s identity. Not just in capital structure, but also in mandate.

In the early days, our board was built for belief. Angels, venture funds, and strategic investors whose job was to back a vision before it was proven. The board’s risk profile essentially matched the founder’s: bet on the builders, stay the course, and survive to fight another day to have a shot at a billion-dollar (or higher) outcome.

When PE investors enter the picture, the calculus changes. PE doesn’t invest in potential; it invests in scalability, predictability, and profitability. The question at the board level shifted from “can you build it?” to “can you scale it profitably, and if so, on what timeline?” The institutional mandate became to fortify the core product, scale the GTM motion, expand margins, and build toward strategic optionality. Everything gets evaluated through that lens.

I understood this intellectually. But what I didn’t fully understand until Q1 2025 is what it would feel like as founder/CEO.

At the time, I was evaluating the board budget and ran into something I hadn’t experienced in nearly a decade of building Jones. It was an inflexibility that I couldn’t find my way around. Not hostility. Not indifference. This was something more disorienting than either: a set of norms and assumptions I didn’t fully recognize, an operating logic I was learning on the fly.

So I approached it the way I’d always handled hard problems with our venture investors. Roll up my sleeves, be transparent about the challenges, ask for advice and genuinely mean it, link arms and solve it together. It was the playbook that had worked for 8 years.

But it didn’t work this time. Not because the board was wrong, or because my approach was flawed. But because I was speaking a language they did not share. They were esteemed scholars in their own PE literature. I was quoting from a different text entirely.

That was the major signal. A quiet, accumulating realization that the company had crossed into a different institutional phase, and my founder operating mode, the one that had worked for so long, was no longer the mother tongue of the room I was standing in.

It wasn’t that my skills had become irrelevant. It was that the company’s needs had become institutionalized, and that specificity started to matter more than the founder’s horsepower and creativity that had gotten us here.

Three signals that it is time to transition

If you’re a founder sitting with this question, wondering whether now is the right moment to welcome a new CEO, here’s a framework I wish someone had handed me in advance of raising a PE round. Your company will send you signals. You just have to know how to read them:

Signal 1: You’re winning on efficiency, not invention

For the first decade of Jones, our edge was creation. We were building a category from scratch, shipping AI products that didn’t exist, and growing by convincing the market that our vision was real. In that phase, the dominant risks were groundbreaking product, remarkable talent, exponential growth, and pure survival. The CEO’s job was fundamentally 0→1.

Once a vertical AI company reaches real institutional scale, the risks change. The business no longer wins primarily on invention. It wins on operational precision. Your best quarters start coming from improved conversion rates and tighter sales cycles rather than new product launches. AI stops being just a product differentiator and starts being a margin lever. For instance, at Jones, we saw a 30% increase in auditing volume alongside an 18% reduction in variable costs, producing a 13% jump in gross margins. Those were the priorities of the PE board.

Yeah, that’s the vibe. And you get used to it.

When this shift happens, the CEO’s job changes fundamentally. You’re no longer primarily an inventor. You’re an organizational designer and systems architect. If you love the former and aren’t naturally wired for the latter two, that asymmetry is worth taking seriously.

Signal 2: The round that changes the question

Here’s the thing about raising from PE: when you’re in the middle of a raise, targeting PE doesn’t feel like an existential question about your role. It feels like the next stage of capitalizing the business. One more chapter that you, the founder/CEO with continued energy and genuine motivation to build, are ready to write.

The term sheet doesn’t come with a warning label. Nobody sends you a note that says “this round may change what leadership this company needs”. You sign, you celebrate, and you keep building. And that’s exactly the blind spot.

Institutional investors have specific performance profiles they’re optimizing for. The question of whether you’re the right person to execute against those expectations is one of the most important acts of leadership. And yet it’s almost never the question you think to work through in the moment.

For Jones, the path forward required three things working in concert. Go-To-Market precision, AI-driven margin expansion, and strategic optionality for the board. Each required operational discipline that favored a PE-focused operator, someone who had navigated the model before and knew which levers to pull and when. I also needed to be honest with myself about whether this was the opportunity that I, as a founder, wanted to spend my time on.

In hindsight, that was clear. In the moment of the raise, it wasn’t what I was asking myself.

The tactical takeaway: before you close a PE round, find a few founders who have been through the same transition, someone post-PE, ideally post-CEO transition, and give them a specific assignment. Have them ask you brutally honest questions about whether you’re truly ready to operate in this new institutional context. Not the questions the term sheet is implicitly answering, but the questions it isn’t asking. You want them to reveal your blind spots.

That conversation, held before you sign the terms sheet, is the one I wish I’d had. Let me be clear: this doesn’t mean I wouldn’t have taken the money. It just means you go into it knowing more clearly what the company needs in the CEO, and whether you are the person for that future role.

Signal 3: You have enough strength to choose

The first signal (that moment in Q1 2025 when I realized I was speaking a different language than my board) wasn’t a call to act immediately. It was a call to awareness.

The lesson isn’t to react the moment something feels off. It’s to recognize the signal, sit with it honestly, and then respond deliberately, with the company’s best interests at the center.

Because your decision isn’t about the founder. It’s about the company.

There’s an adage in tech and venture capital: always raise from a position of strength. It’s frustrating advice, as most often you’re not in that position. But it’s true. The same logic applies here. Founders should lead CEO transitions from a position of strength, and more importantly, they should actively manufacture the conditions for that window to exist.

That means continuing to perform well. Crush the board milestones. Get the team, the product, and the balance sheet into the best shape you can before you start the conversation. Because these conditions matter enormously. A new CEO walking into a business with momentum can attract great talent, earn the team’s trust faster, and build on what’s already working. A new CEO walking into a business under pressure is immediately playing defense.

We hit our window in late 2025. Record quarters. A healthy balance sheet. A world-class AI product in the market. A team that had proven it could execute at scale. That strength wasn’t incidental — it was the prerequisite. This gave our new CEO a running start and the company the best possible chance of making the transition work.

Founders owe this to the company, to their team, and to their investors. It’s not only stewardship. It’s the fiduciary duty. And it’s simply the right thing to do.

The mechanics of a clean CEO transition

Most people don’t write about “how” to transition. Once you’ve made the decision, the work of making it real begins.

We organized the transition around three layers: downloading founder intuition, handing off ownership, and aligning on the future.

Layer 1: Downloading founder intuition

For 8 years, most of the Jones strategy lived inside my head: Product strategy and logic, customer nuance, the cultural DNA. There was context behind every major decision that never made it into a slide deck. That tribal knowledge is an asset, and in a poorly structured transition, it evaporates. Here are two examples:

The Product Vision: Our new CEO and I spent hours on the logic behind our AI roadmap; not just what we’re building, but why, and which parts of the vision are non-negotiable if we want to keep winning the category. We put that in writing. Not as a manifesto, but as a working onboarding document that the new CEO can interrogate, evolve, and reference when the inevitable trade-off decisions arrive.

The Leadership Map: You can’t inherit a 231-person culture from an org chart. We mapped the key leaders and cultural carriers across the business, the people who shape how others think and behave, regardless of their formal title or seniority. Then we assessed where the incoming CEO’s operating style aligns with that culture, and where friction is likely to emerge. We also flew to every geographic hub to spend time with key leaders, both formally and informally. Getting honest about that gap early is far less expensive than discovering it at month four.

Layer 2: Handing off ownership

The fastest way to break a winning company is through ambiguous leadership. During a transition, if the team receives two different signals from two different leaders, execution stalls. We were deliberate about preventing that from day one.

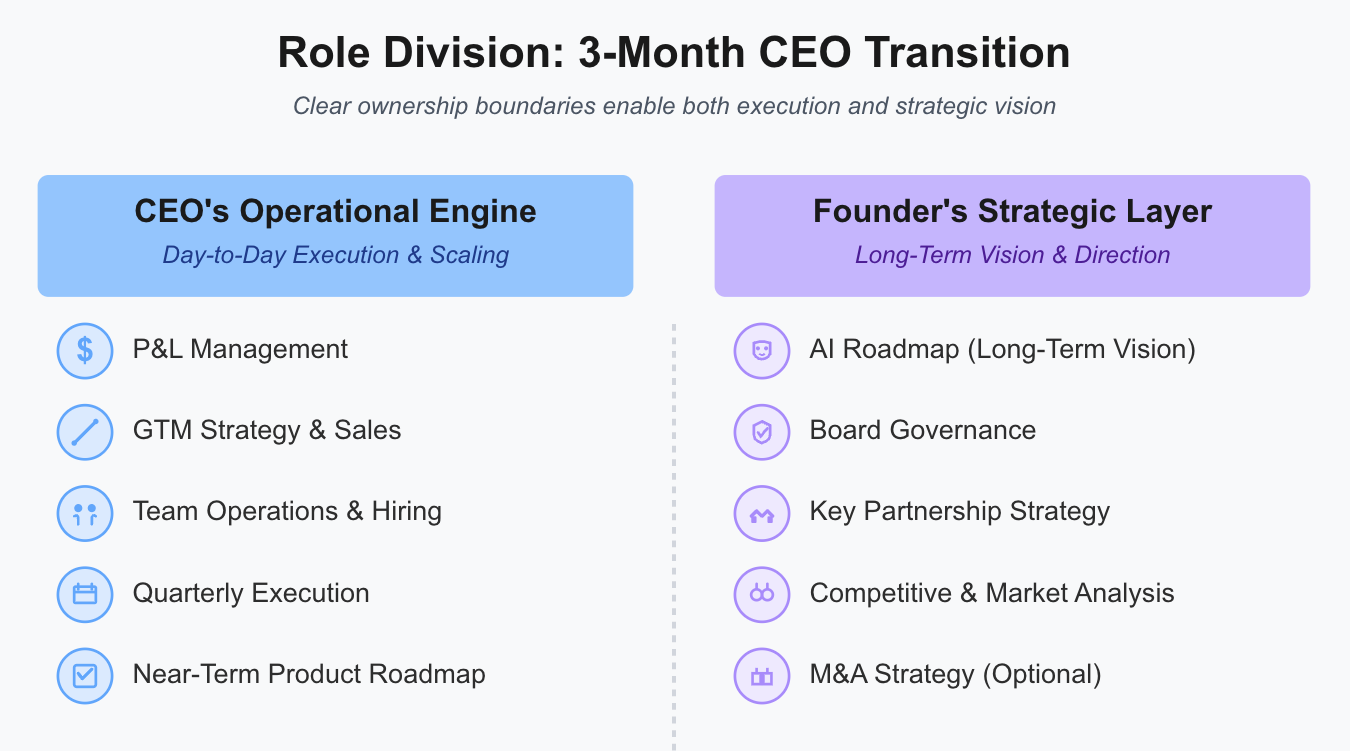

We built a 3-month transition framework for this around two principles. First, autonomy: the incoming CEO owns the P&L, the GTM machinery, headcount and hiring, and the day-to-day operating rhythm – full stop. The team needed to know clearly and consistently that the buck stops with them, from day one.

Second, high-leverage focus. My role shifted to the areas where founder context provides irreplaceable value: areas like board governance, strategic partnerships, and our long-term AI roadmap.

The tactical takeaway is to map the founder’s domain and the CEO’s domain before you start the transition. Don’t leave it to evolve organically. Name it explicitly, put it in writing, explain it to your team, and revisit it at the 30, 60, and 90-day marks.

Layer 3: Aligning on the future

In a founder-led company, the team’s belief in the mission is often an extension of their belief in the founder. That trust doesn’t transfer automatically with a C-suite change. Trust has to be earned, and the founder has to actively enable the conditions for that to happen.

So to build that trust, we were intentional about three things:

First, co-signing the early moves: During the transition, we were deliberate about co-signing major strategic initiatives so the team sees that the new CEO’s decisions are a direct evolution of the vision, not a departure from it.

Second, explicit advocacy: My job during the succession was to be our new CEO’s most vocal advocate, specifically articulating why his superpowers were exactly what Jones needed for the new chapter.

Third, passing the mic: In meetings where I once led, I sat in the active listener seat. The new CEO took the final word, I provided historical context in the room and in post-meeting debriefs. This is harder than it sounds when you have strong opinions and years of context. But it’s the only way the team learns to orient toward the new leader.

Put the company ahead of yourself

Everything I’ve described — reading the signals, manufacturing the window, executing the handoff — requires putting the company ahead of yourself at every step. That’s not a minor ask.

That’s because founders are taught to think of themselves as the irreplaceable force holding everything together. And there’s truth in that, especially in the early years. But that narrative can become a trap.

The ultimate act of leading a company is not building something that depends on you. It’s building something bigger than you. Bringing on specialized leadership isn’t a retreat from that mission. Done right, it’s the fullest expression of it, a deliberate bet that the company’s future is too important to be constrained by any one person’s fixed set of skills, including your own.

The founder/CEO can leave, and that’s often how you build something that endures. But at the same time, the connective tissue, the values, and the tribal knowledge have to stay. When you’ve built something that holds together without you, you’ve succeeded, even if it feels like a loss.

If you are a CEO considering a transition, or whether it is time for new leadership, please don’t hesitate to reach out.

Key takeaways

The best time for a founder CEO transition is when the company is winning, not when it’s struggling. Strength gives the new CEO a running start.

PE investment changes the institutional mandate. The skills that got you here (invention, vision, survival) may not be what the next phase requires (operational precision, margin expansion, scalability).

Three signals it’s time: you’re winning on efficiency rather than invention, you’ve raised a round that changes the question, and you have enough strength to choose deliberately.

A clean transition has three layers: downloading founder intuition into working documents, handing off ownership with zero ambiguity, and actively enabling the new CEO to earn the team’s trust.

The ultimate act of founder leadership is building something bigger than yourself, and knowing when specialized leadership serves that mission better than you can.

| A guest post by

|