6 patterns that kill startups (and how to overcome them)

These patterns show up in almost every startup. Don’t let them kill yours.

I spent four years and $7 million building Workstream.io. I pivoted four times, experimented with dozens of ICP variations, and genuinely believed I was doing everything right.

When I finally shut it down in April 2024, I came out the other side feeling something I hadn’t expected: clarity. But not immediately.

First came the grief, the self-doubt, the long stretches of reflection. But eventually, there was clarity. And with it, a burning need to understand not just why my company failed, but why so many of us fail; and what we can actually do about it.

That’s what drove me to start Not Another CEO. For the last two years, I’ve spent my days coaching founders and CEOs, building Founder/CEO communities in New York and Atlanta, and studying failure patterns across hundreds of startup journeys. Not the polished post-mortems. The real stuff: the conversations with founders mid-crisis, the pattern recognition that comes from sitting with dozens of people all facing versions of the same problems.

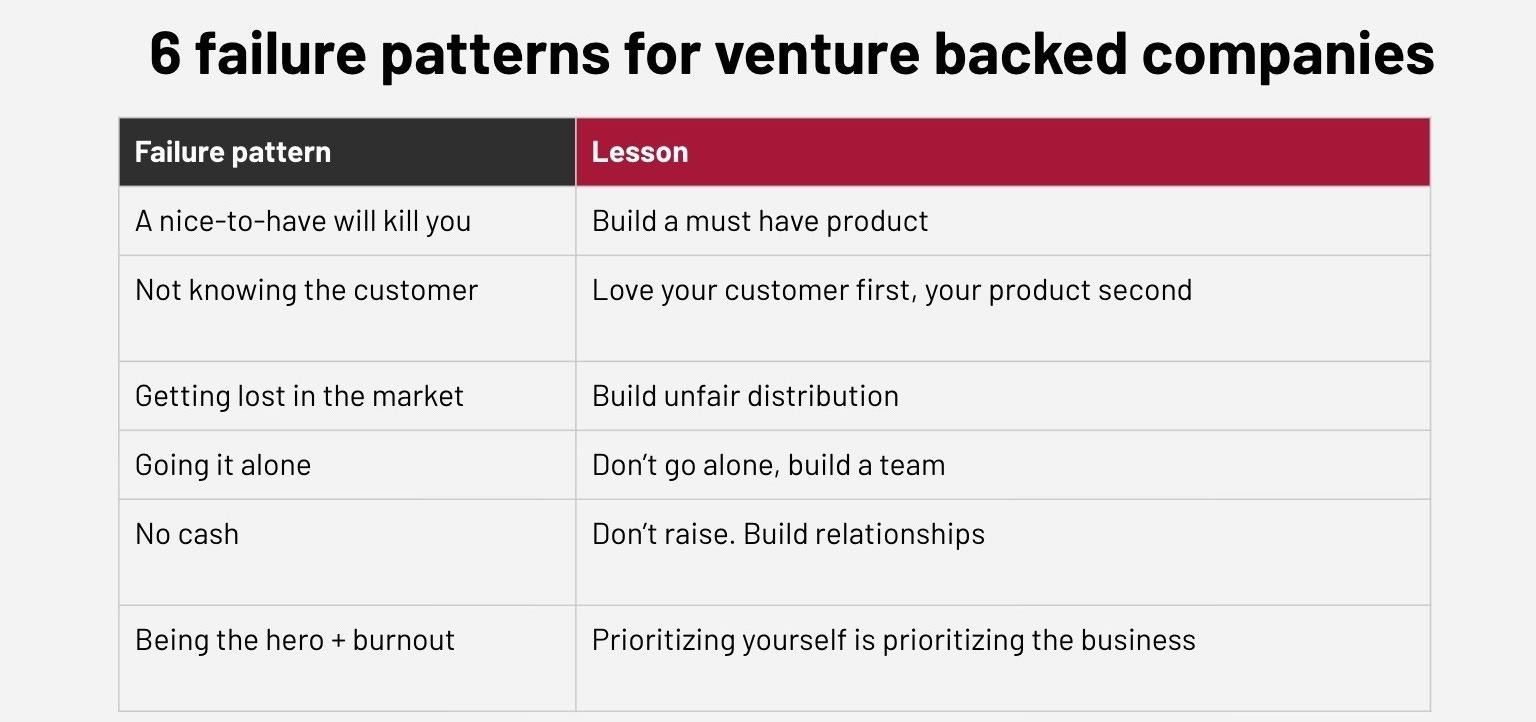

Here’s what I’ve found: most companies don’t fail for unique reasons. They fail for the same six reasons, over and over again.

Some are obvious. Some are subtle. All of them are survivable if you catch them in time. And most founders, when they’re honest with themselves, already know which ones apply to them.

I shared these six patterns with a room full of founders recently, and I want to share them with you.

Table of contents

Pattern #1: A nice-to-have product will kill you

Pattern #2: Not knowing the customer

Pattern #3: Getting lost in the market

Pattern #4: Going it alone

Pattern #5: Running out of cash

Pattern #6: Trying to be a hero and burning out

Pattern #1: A nice-to-have product will kill you

This one killed my company. And it kills most companies. 42% of failed founders say that their primary cause of failure is not solving a big enough problem (CB Insights). 52% of failures are due to a lack of product-market fit. (Failory)

But the generic use of the phrase “lack of product-market fit,” I think, sanitizes what is actually a slow, painful spiral that often lulls founders into a sense of comfort (and complacency).

The more precise version is: you have a nice-to-have product, not a must-have. People might think your product is interesting, but that’s not enough. And a nice-to-have will bleed you dry before you ever figure out what went wrong.

Peter Thiel said it best:

“Proprietary technology must be at least 10× better than its closest substitute in some important dimension… anything less… will be perceived as a marginal improvement and will be hard to sell.”

The 10X bar sounds extreme until you consider the friction you’re asking customers to overcome: switching costs, internal buy-in, budget justification, and the inertia of doing nothing. If your product doesn’t clear all of that, you’re in trouble.

As founders, we rarely hold ourselves to a high enough standard here, and so we experience a more subtle and dangerous version of this problem. Ted Conbeer, who was SVP of Data & Strategy at Makespace, was a longtime design partner of mine and is now the Founder of the data consultancy Shandy, put it this way: “The death zone of any startup isn’t no traction at all. It is just a little bit of traction.”

I lived in that death zone for years. Just enough signal to believe that one more feature, one more pivot, or one more push was all I needed. It lulls you into feeling like you’re almost there; the finish line is just one more release away.

Near the end of my journey, a longtime friend and customer named Edmund Helmer (then Director of Analytics at Mountaintop Studios, formerly at Meta/Oculus), gave me this blunt feedback: “The value of Workstream.io is greater than the hassle of adopting a new system/cost. But I need the value to be many times greater than the hassle.” The ratio wasn’t there. People saw the value. They just didn’t need it badly enough to fight for it.

So what is the lesson here?

A must-have product solves your customer’s number one problem and is 10x better than any alternative, including doing nothing.

If you’re not there, or do not know, you need to find out fast: not through surface-level validation, but through hard conversations where you ask your customers to tell you. Are you “interesting” (a nice to have) or “valuable” (a must have)? Are you solving their #1 problem? If so, why not, and why are you potentially wasting your time on something else?

If you feel like you don’t know whether you’re building a must-have product, you probably aren’t. Trust that feeling. I didn’t, and it cost me everything I’d built.

Interested in chatting one-on-one about this? Schedule a call with me.

Pattern #2: Not knowing the customer

The six patterns will feel more obvious to start, but become subtler and more difficult to discern as we go.

Not knowing the customer is less obvious than pattern #1, but it’s usually the cause.

Before starting Workstream.io, I had nearly a decade of experience in high-growth companies. I was employee 200 and pre-revenue at Tesla. I was employee 12 at BetterCloud and ran Operations while serving on the ELT, growing from zero to $50M in ARR and nearly 500 employees. I thought I was the most prepared first-time founder ever. I was so arrogant that I actually told investors that; these were investors whose money I later lost.

My confidence was real, but it was misplaced. I had proximity to and experience with a problem. But I was missing what Brian Chesky, paraphrasing something from Paul Graham, captures simply:

“It’s better to have 100 people love you than a million people that just sort of like you.”

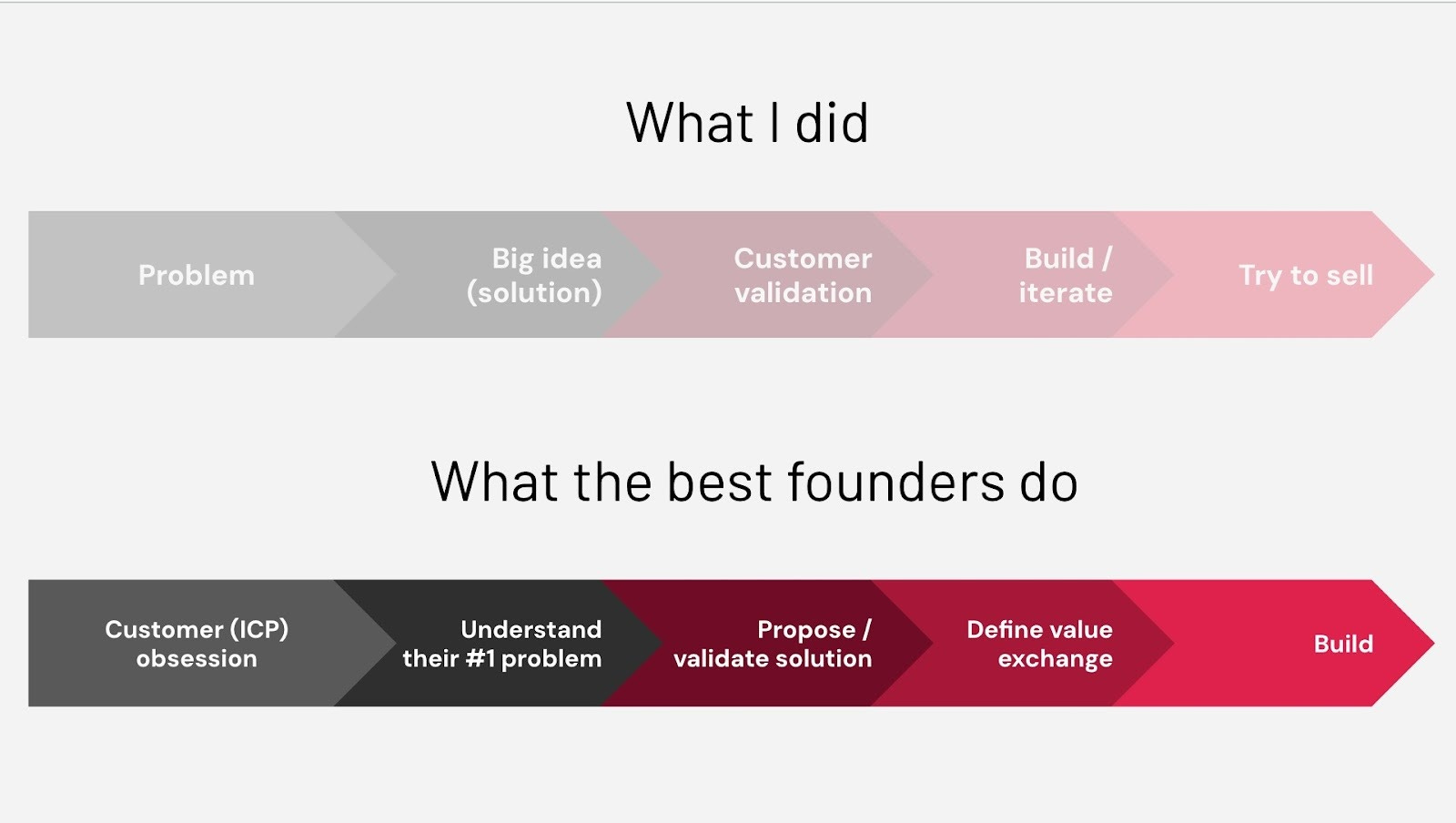

The conventional startup playbook sounds straightforward: identify a problem, validate with customer interviews, build an MVP, iterate. Most of us follow this, but it is wrong. Think about it: we start with an idea, and then we go look for customers to confirm it. That’s backwards.

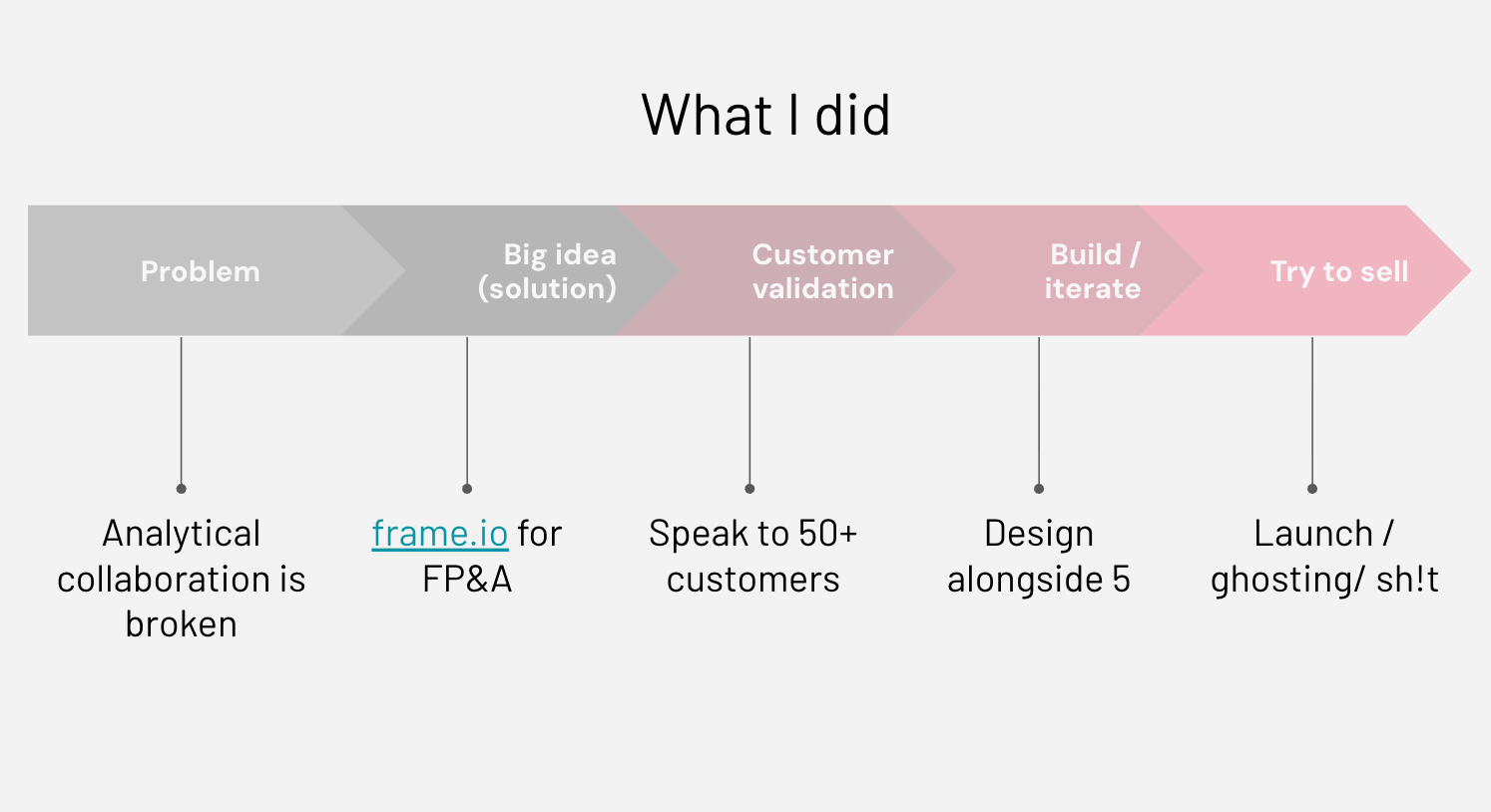

I did exactly this. I had a vision for “Frame.io for FP&A.” (Frame.io got bought for $1B by Adobe, that sounds great - let’s go build that!) I quit my job, spent six months talking to 50+ potential customers, found five design partners, and launched an alpha.

What happened next? Ghosting; years of pivots, imposter syndrome, and living in the sh!t, wondering where I’d gone wrong.

The problem wasn’t my process. It was my sequence.

The best founders start with an obsession about a specific person. Not “data analysts” — something hyper-focused like: engineers at mid-market SaaS companies experiencing hypergrowth and managing Kubernetes. (And that is actually nowhere near specific enough).

These founders become almost unreasonably curious about that person’s world and passionate about serving them before they think about what to build. Kyle Porter, founder and CEO of Salesloft, described his approach: “Our original mission was to do everything that we can to help our customers sell better, period, even if it has nothing to do with the product.”

Diego Oppenheimer, founder of Algorithmia, kept it even simpler: “Don’t forget who pays for lunch. It’s the customers!”

I have known Curtis Lee, co-founder and CEO of Luxe and co-founder of Pinwheel, since before I started my company. Early in my journey, he asked me a question which I wish I had thought more about at the time: “How much do you love your customers? You are going to spend a lot of time with them.”

He wasn’t being sentimental. You are going to spend five, ten, maybe fifteen years in service to these people. If you don’t love them — not the product, not the mission, them — you will not go the distance.

Love your customer first, and your product second. Everything else is a distant third.

Pattern #3: Getting lost in the market

This one trips up founders who have gotten many of the other things right. You’ve built something real for customers whom you understand. And you still can’t grow.

This is another lesson I learned the hard way: startup best practices ≠ success. I read all the right books, including the Lean Startup. We had four major pivots and dozens of micropivots based on real customer signals. I iterated across dozens of definitions of my ideal customer profile and ideal buyer personas.

And when we finally found product market fit after years, I watched with anxiety as my company disappeared into the market.

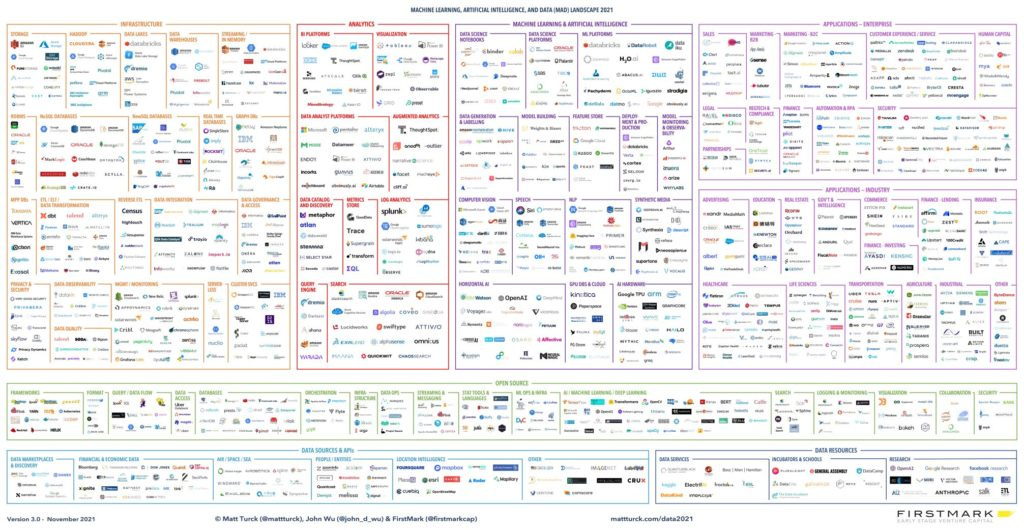

Can you find the Workstream.io logo in the above MAD Landscape? (This is the 2021 version of the annual market map FirstMark Capital publishes, charting every company in the data space). There is so much competition that finding any individual company is nearly impossible. I’m still not sure if we are even on here.

That was my market, and in today’s venture landscape, where there is more capital and it is easier to build products and companies than ever before, dozens of companies are pursuing almost every market and segment. And here is the brutal truth: like most founders, I had spent almost all of my energy on the product rather than figuring out how to be found.

Ben Sun, co-founder of Primary Ventures and former CEO of Community Connect, puts it plainly: “When people come to me, they’re thinking like 90% product and 10% distribution. You’re most likely going to fail, because customers just have so many options out there. If you’re not spending at least 50% of your energy thinking about distribution, you’re going to struggle.”

The companies that break out of crowded markets don’t just have better products. They have unfair distribution advantages: structural reasons why they can reach their customers in ways competitors can’t replicate.

Take Omni, a BI company founded in 2022 (full disclosure: I am a small investor). Co-founders Jamie Davidson and Colin Zima had spent years as senior executives at Looker and then at Google Cloud. When they started Omni, they already had a detailed, vetted product roadmap, and just as important, they already knew exactly who their ideal customers were. When I spoke to Jamie before they closed their Seed, he told me: “We know exactly what we are building, and who our customers are.” The result: $30M ARR by 2025 and still doubling.

You could claim that this unfair advantage was given, not built. But take dbt Labs: before they were a pure-play product company, they were Fishtown Analytics, a bootstrapped data services firm, for four years.

By the time they raised their Series A, dbt Labs had a Slack community of 5k members, 1.7K companies using their open-source solution, and 250 paying hosted customers. They had the love of thousands of customers, from whose cold, dead hands you could not rip dbt. dbt Labs spent years bootstrapping a distribution engine nobody could replicate.

Your company does not need to be born with unfair distribution advantages; you can build this too. But you have to be intentional about it from day one. Not as an afterthought once the product is ready. If you’re spending 90%+ of your time on product, start asking yourself why.

Pattern #4: Going it alone

We all know the current narrative in tech: in the age of AI, solo founders are becoming more common. Founding teams are getting smaller. According to Carta, 36% of US startups are solo-founded today, up from less than 24% in 2019. Founding teams can also build more with less, so they are waiting longer to make their first hires.

And while the data shows all of that to be true, it is hard to reconcile with the reality that most founders experience. Such as what Nadia Boujarwah, co-founder and CEO of Dia & Co, says about the resiliency required to build a company over 12+ years: “It’s just different with a co-founder.”

That’s it. No elaboration needed. Toby Kraus, co-founder and CEO of Lightship (the electric RV company that’s raised $60 million), makes it even more concrete: “You usually run out of emotional runway before you run out of cash runway.”

Sit with that. This is an exceptional statement from a CEO who is building one of the most cash-intensive businesses you can imagine. The cumulative weight of making consequential decisions under uncertainty, alone, over multiple years, is far more likely to kill your company than running out of cash.

I recently saw this destroy a company that should have made it. The CEO of an open-source company spoke to me about how they quickly hit 10K+ stars on GitHub and raised $11M in Seed funding. But as it turned out, open-source traction didn’t yield monetization, and the journey quickly became difficult.

They successfully pivoted, were customer-obsessed, and their new product was working. The CEO had a bridge lined up. But then his co-founder and CTO called him and said he was done. He no longer had the energy. The CEO’s reply? “I can’t do this without you.”

They shut it down. Not because they were out of cash, not because of traction, but because they were out of energy.

Like Phil Fernandez, founder and CEO of Marketo, says: “Hiring and staffing…is like assembling an orchestra or putting together a symphony…where things play off of each other, people adapt.” So when assembling your team, don’t forget that you want them to take you across the finish of the marathon, not just sprint to your first milestone.

As the African proverb says: If you want to go fast, go alone. If you want to go far, go together.

Pattern #5: Running out of cash

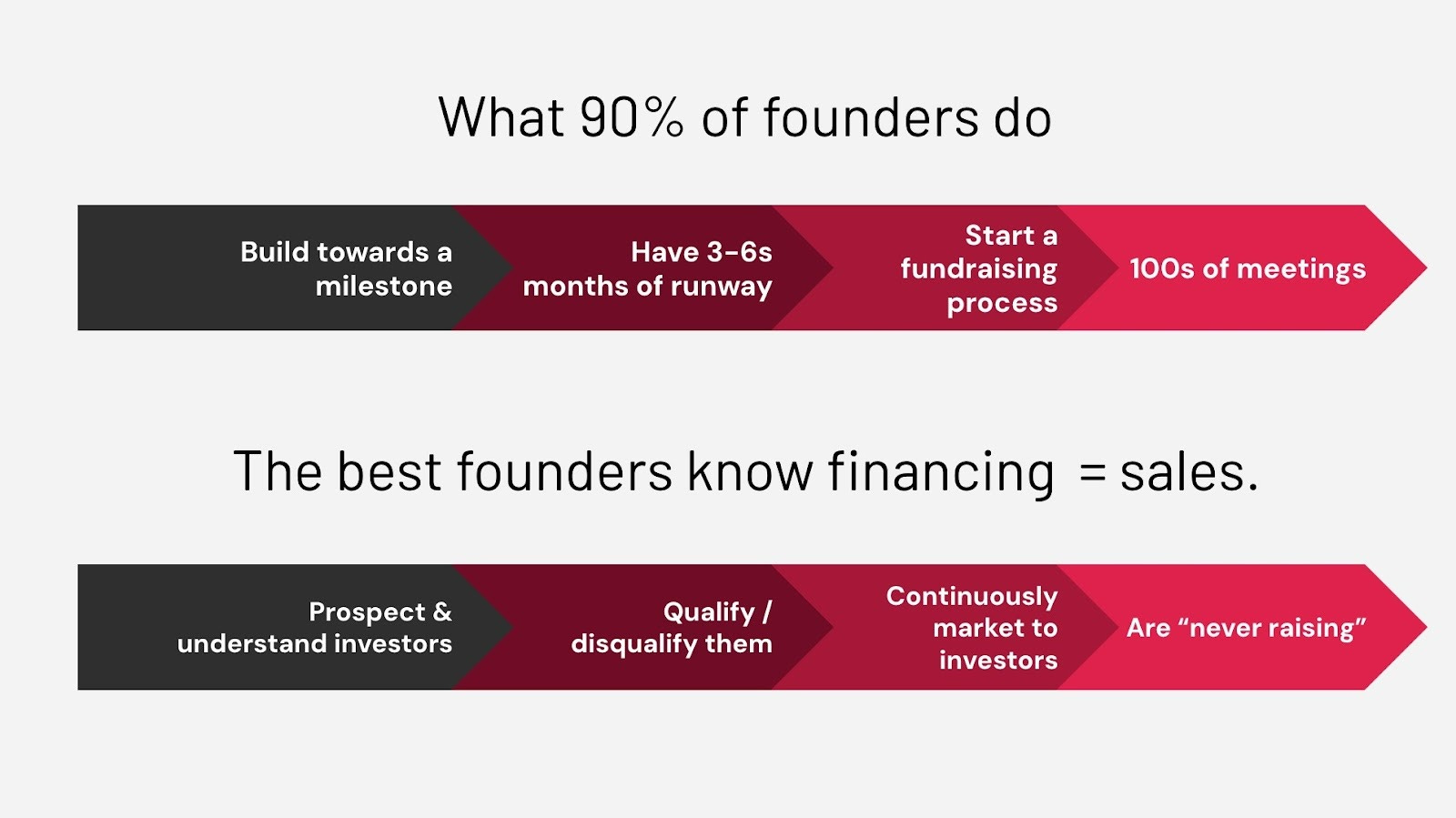

When you talk about startup failure, this is the end state that we always think about: running out of cash. But how founders get here is wildly misunderstood.

Here is my own quote, a joke I made up when running Finance for the Model S Program. “Don’t forget the three rules of startup finance. 1) Don’t run out of cash. 2) Don’t run out of cash. 3) When in doubt, refer to rule #1.”

While we did shut down Workstream.io, it was not actually because I was bad at financing. I’m actually quite good at it, but many founders struggle with it, no matter how compelling their business and traction.

As Jindou Lee, founder and CEO of Happy Co, describes it: “Fundraising is a very unfair game for founders. A founder may raise three times, four times…maybe six at best…we’re playing a game against people that invest for a living.”

How do most founders approach fundraising? We build toward a milestone and hopefully get there with six months of runway to spare. We start a process, take hundreds of meetings, and hope for a term sheet before the lights go out.

I was recently speaking with a CEO who had gone from zero to $250K in ARR in 60 days. They had traction with some great customers, and pipeline momentum was accelerating. But she was starting to raise funds with less than 90 days of runway and no strong leads or relationships. She had three options: pray for a term sheet, put in more of her own money, or shut down.

That is not a negotiating position. That is a crisis.

The best founders think about fundraising differently. Mike Lazerow, founder of Buddy Media, described how he and his cofounder, Kass, built genuine investor relationships:

We kept them in the loop. We would send them quarterly updates…we’d learn about their interests and look for ways we could add value to their world…if we liked each other, they would jump when opportunities arose…and we could negotiate from a relational foundation.”

Don’t forget: financing is sales. The work happens long before you ask for the deal. The best founders are always in the market; they are “never raising” but they’re always meeting with prospective investors, qualifying them, and staying in front of them. They’re building relationships.

At Workstream.io, I took an inbound meeting from Lerer Hippeau two years before they invested. Many founders would not have taken the meeting, as at the time, their reputation was of a consumer-focused fund. They weren’t an obvious fit for a data workflow company. But over two years of conversations, I learned they were actively diversifying into enterprise, and they learned about me and my co-founder Chris, saw all the ups and downs of our journey, and bought into our vision and resiliency as a team.

By the time I raised a Seed, the relationship was already there: I called them first, and they led our round.

The best time to talk to investors is when you don’t need them.

Pattern #6: Trying to be the hero and burning out

This pattern is the one I am most passionate about writing about. It’s personal.

Based on a report published by Michael Freeman, the data on founder mental health is scary:

72% of founders report some form of mental health concern. 49% have at least one identified mental health condition — 32% have two or more. 23% come from families with highly symptomatic mental health histories.

I’m in that last group.

So, as a group, founders step into our role with a less-than-ideal mental health track record. And what is it that we choose? What Chieh Huang, co-founder and CEO of Boxed, describes as “like trying to be the greatest of all time in a broken glass eating competition.”

This journey we choose is incredibly painful; in your company’s best times, the demands put on you are immense, and the expectations for success are extraordinary. It is just stressful, and not many people will have sympathy for you.

As Adam Dell, Founder/CEO of Domain Money, says: “Your team has no conception of how lonely it is.” Your pain is real, unceasing, and largely invisible to everyone around you.

My third child was born during one of the most critical pushes at Workstream: as we were monetizing our flagship product. I was genuinely scared: both for the health of my wife and my newborn daughter. We weren’t getting much sleep. And if that wasn’t enough, a week after my daughter was born, my brother, a co-founder of Bleacher Report, someone who had struggled with mental health for years, passed away.

I was navigating the most acute grief of my life while trying to hold a company together and present to my team, my customers, and my investors that I had it under control.

I’m not sharing this to garner sympathy. I’m sharing it because we don’t talk about this enough, even though most founders experience these difficult times. We’re just mostly silent about the very real human cost of what we’re doing.

So what are we to do as founders? I think it is important to be painfully honest about your drivers for entrepreneurship: the good and the bad. Most founders have mission-driven reasons for doing what they do, but the less healthy drivers, such as fame, power, money, and authority, are often just as prevalent.

Second, we need to recognize that no matter how hard we work, we cannot control our outcome and whether we will get what we seek. All that is certain, as my close friend and brother’s cofounder Dave Finocchio at Bleacher Report once told me, is that it is “about the journey.”

When he told me this, I thought he meant that through the journey, you create amazing memories, and that is what you remember at the end. And while that is true, what he actually meant was far more profound.

First: no matter the result, the journey will change you. Only you get to choose how. Make sure it changes you for the better.

Second: because the journey is so hard, so lonely, and so uncertain, you must savor the journey each day you live it. You need to make the joy you receive each day worth the pain and loneliness.

This is all very hard. As Tony Safoian, CEO of SADA, describes the “energy management required to be a great husband, father, and great CEO...it’s almost superhuman. So you have to behave as if you’re training for the Olympics all the time.”

Professional athletes have a whole system of trainers, nutritionists, managers and coaches designed to support them. So here is the final lesson:

Taking care of yourself and building your support system are not distractions from building your company. It is the company. Because without it, you don’t survive long enough to build anything.

Trust your gut

These six patterns – building a nice-to-have, not knowing your customer, getting lost in the market, going it alone, running out of cash, trying to be the hero – show up in almost every company. Often in combination. Sometimes all at once.

I’m confident that at least one of them applies to you right now. And if you don’t take action, that will be enough to kill you.

So there are two things I will leave you with:

First, trust your gut. Every founder I’ve ever spoken with knew something was wrong before they admitted it. Your instincts in these areas are almost always right. When your spidey senses start firing, listen to them.

Second, say something and do something about it. Tell your co-founder. Tell a board member. Tell someone in your support system.

And if you feel like you have no one to talk to about it, reach out to me.

Key takeaways

A nice-to-have product is a death sentence. If you’re not solving your customer’s #1 problem and doing it 10x better than the alternative, you’re in the death zone.

Start with the customer, not the idea. The best founders are obsessed with a specific type of customer before they ever think about what to build.

Distribution is not an afterthought. If you’re spending 90% of your energy on product development, you’re likely to get lost in the market, no matter how good your product is.

You’ll run out of emotional runway before cash runway. Building alone is a liability. Your team is your resilience infrastructure.

Fundraising is sales. The best founders are always thinking about the next fundraising round, connecting with and qualifying potential investors.

Taking care of yourself is taking care of the business. You can’t build anything if you don’t survive long enough to see it through.

Incredibly helpful article! Thank you Nicholas!

Love this article Nicholas - feels like brutal honesty in world where you can get seriously overwhelmed by the many "we went from zero to a gazillion in 12 months" insta-like stories about start-ups.